Taxability: SSDI benefits can be taxable if your combined income exceeds specific thresholds ($25,000 for single filers and $32,000 for joint filers).

Tax Thresholds: Up to 50% of SSDI benefits may be taxable if your combined income falls between $25,000 and $34,000 for single filers or between $32,000 and $44,000 for joint filers. Up to 85% of SSDI benefits may be taxable if your combined income exceeds $34,000 for single filers or $44,000 for joint filers.

Reporting Requirements: SSDI benefits are reported on Form 1040, with the total amount on line 5a and the taxable amount on line 5b.

Answer: Yes, SSDI benefits can be taxable, but only if your combined income exceeds specific thresholds.

However, most SSDI recipients do not pay taxes on their SSDI benefits because their income levels are typically low.

The taxability of SSDI benefits depends on the recipient’s combined income, which includes half of their SSDI benefits plus all other income and tax-exempt interest.

If this combined income exceeds specific thresholds, a portion of the SSDI benefits may be subject to taxation.

Overview of Social Security Disability Insurance (SSDI)

Social Security Disability Insurance (SSDI) benefits are a form of federal assistance provided to individuals who have worked and paid Social Security taxes but are now unable to work due to a disability.

The primary purpose of SSDI is to provide financial support to those who have contributed to the Social Security system through their work history and are now unable to earn a living due to a severe medical condition that is expected to last at least one year or result in death.

If you or a loved one have questions about the tax implications of your SSDI benefits or need guidance with the SSDI eligibility process, you can use the chat on this page to connect with an experienced SSDI attorney at TruLaw.

Our team offers a free, no-obligation consultation and is available to answer any questions you may have about your SSDI benefits and potential tax obligations.

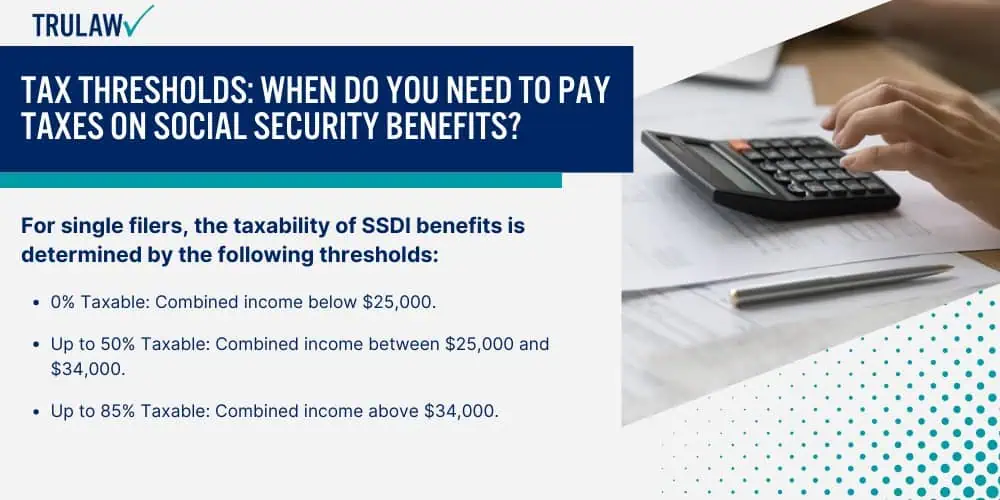

Tax Thresholds: When Do You Need to Pay Taxes on Social Security Benefits?

The taxability of SSDI benefits depends on the recipient’s combined income, which includes half of their SSDI benefits plus all other income and tax-exempt interest.

Below, we’ll discuss how tax thresholds differ based on the filing status of the SSDI recipient.

Single Filers

For single filers, the taxability of SSDI benefits is determined by the following thresholds:

0% Taxable: Combined income below $25,000.

Up to 50% Taxable: Combined income between $25,000 and $34,000.

Up to 85% Taxable: Combined income above $34,000.

Joint Filers

For married couples filing jointly, the taxability of SSDI benefits is determined by the following thresholds:

0% Taxable: Combined income below $32,000.

Up to 50% Taxable: Combined income between $32,000 and $44,000.

If married individuals file separately and lived with their spouse at any time during the tax year, their SSDI benefits may be fully taxable.

This means that there is no exemption threshold, and all SSDI benefits received may be subject to taxation.

Recognizing these tax thresholds is important for SSDI recipients to identify whether their benefits are taxable and to what degree.

It’s important to note that these thresholds apply to your combined income, which includes half of the SSDI benefits plus all other income and tax-exempt interest.

If you or a loved one are uncertain about how tax thresholds affect your SSDI benefits or need help with the tax implications of your benefits, you can use the chat on this page to connect with an experienced SSDI attorney.

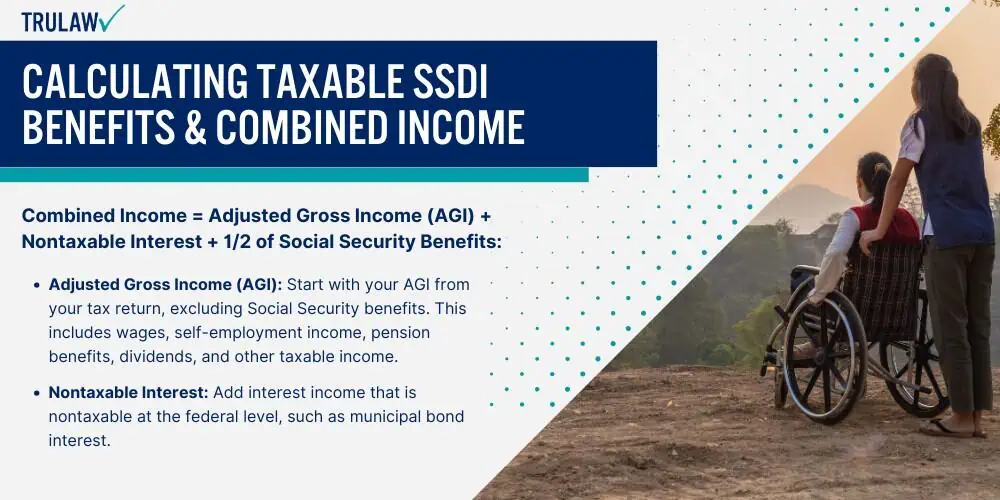

Calculating Taxable SSDI Benefits & Combined Income

To determine if your SSDI benefits are taxable and to what extent, you need to calculate your combined income.

Combined income includes half of your SSDI benefits plus all other income and tax-exempt interest.

Below, we’ll walk you through the formula used to calculate what your combined income is.

Combined Income = Adjusted Gross Income (AGI) + Nontaxable Interest + 1/2 of Social Security Benefits:

Adjusted Gross Income (AGI): Start with your AGI from your tax return, excluding Social Security benefits. This includes wages, self-employment income, pension benefits, dividends, and other taxable income.

Nontaxable Interest: Add interest income that is nontaxable at the federal level, such as municipal bond interest.

Half of Social Security Benefits: Add half of the Social Security benefits from your Form SSA-1099.

Calculating Taxable SSDI Benefits (Example)

Let’s consider the following scenario:

Combined Income: A single filer has a combined income of $30,000.

SSDI Benefits: Their SSDI benefits are $20,000.

Threshold: The threshold for 50% taxability is $25,000.

Step #1: Determine the Difference

Start by calculating the difference between the combined income and the threshold:

Combined Income: $30,000

Threshold: $25,000

Difference: $30,000 – $25,000 = $5,000

Step #2: Calculate the Taxable Amount

The taxable SSDI amount is half of this difference — up to 50% of the SSDI benefits received:

Difference: $5,000

Taxable Amount: $5,000 / 2 = $2,500

Step #3: Verify the Taxable Amount

Confirm that the taxable amount does not exceed 50% of the SSDI benefits received:

SSDI Benefits: $20,000

50% of SSDI Benefits: $20,000 * 0.5 = $10,000

Because $2,500 is less than $10,000, the taxable amount of $2,500 is confirmed.

In this example, the single filer with a combined income of $30,000 and SSDI benefits of $20,000 has a taxable SSDI amount of $2,500.

This is half of the difference between their combined income and their tax threshold (up to 50% of their SSDI benefits).

For other detailed calculations and specific examples, refer to IRS Publication 915 or consult with a tax professional.

If you or a loved one need help calculating the taxable portion of your SSDI benefits or have questions about how combined income affects your tax situation, you can use the chat on this page to connect with an experienced SSDI attorney.

Our team provides a free, no-obligation consultation and is ready to address any questions you may have regarding your SSDI benefits and potential tax responsibilities.

This form shows the total amount of SSDI benefits received by that recipient during the previous year.

It is important to review this form carefully to ensure that the information is accurate and complete.

You should receive this form by January 31st of each year, so be sure to keep an eye out for it in your mailbox.

Step 2: Report Total SSDI Benefits on Form 1040

By accurately reporting your SSDI benefits on Form 1040, you can ensure compliance with tax regulations and avoid any potential issues with your tax return.

To report SSDI benefits on your tax return, follow these steps:

Find the Total Amount: Look for the total amount of SSDI benefits on Box 5 of Form SSA-1099.

Enter on Form 1040: Report this total amount on line 5a of Form 1040 or Form 1040-SR.

Step 3: Calculate Taxable SSDI Benefits

Not all SSDI benefits are subject to taxation.

The portion of your benefits that is taxable depends on your income and filing status.

To determine the taxable amount of your SSDI benefits, follow these steps:

Use the Social Security Benefits Worksheet: Complete the Social Security Benefits Worksheet (lines 5a and 5b) to determine the taxable portion of your SSDI benefits.

Enter Taxable Amount: Report the taxable amount on line 5b of Form 1040 or Form 1040-SR.

Example of this Process

To illustrate this process, let’s consider the following example.

Suppose an SSDI recipient receives their Form SSA-1099 and needs to report their benefits on their tax return.

Total SSDI Benefits: Found in Box 5 of Form SSA-1099, the recipient sees that their SSDI benefits for the previous year totaled $20,000.

Enter on Line 5a: They would then report $20,000 on line 5a of Form 1040 or Form 1040-SR.

Calculate Taxable Amount: Next, they would use the Social Security Benefits Worksheet to determine the taxable portion of their benefits — for this example let’s say it’s $2,500.

Enter on Line 5b: They would then report $2,500 on line 5b of Form 1040 or Form 1040-SR.

If you or a loved one need assistance with reporting SSDI benefits on your tax return or have questions about the tax implications of your benefits, you can use the chat on this page to connect with an experienced SSDI attorney.

Our team offers a free, no-obligation consultation and is available to answer any questions you may have about accurately reporting your SSDI benefits and minimizing your tax liability.

While the federal government may tax SSDI benefits under certain conditions, state taxation of SSDI benefits varies from state to state.

Most states do not tax SSDI benefits, but it’s important to review your state’s specific laws to identify any potential tax obligations.

It’s important to note that even in states that tax SSDI benefits, not all benefits are taxable, and the amount subject to taxation can vary based on income and filing status.

State taxation policies can change, so it’s important to stay informed about the current rules in your state.

Always consult with a tax professional or check with your state’s tax department to gain clarity on the specific rules and any potential tax obligations.

States That Tax SSDI

As of 2024, the following states tax (or previously taxed) SSDI benefits to some extent:

Colorado: Colorado taxes SSDI benefits for taxpayers at a flat rate of 4.4% for those under 65. Individuals 65 and older can deduct federally taxable SSDI benefits from their state taxable income. Those aged 55 to 64 can deduct up to $20,000 in retirement income, including SSDI.

Connecticut: Connecticut taxes SSDI benefits if adjusted gross income (AGI) exceeds $75,000 for single filers or $100,000 for joint filers. Above these thresholds, 75% of SSDI benefits are tax-exempt.

New Mexico: New Mexico taxes SSDI benefits at a rate of 1.7% to 5.9% for taxpayers with incomes over $100,000 ($75,000 if married filing separately or $150,000 if a qualifying surviving spouse, head of household, or married filing jointly).

Rhode Island: Rhode Island taxes SSDI benefits at a rate of 3.75% to 5.99% if AGI exceeds $101,000 for single filers or $126,250 for joint filers.

Utah: Utah taxes SSDI benefits for taxpayers with incomes over $45,000 ($75,000 if head of household or married filing jointly).

Vermont: Vermont taxes SSDI benefits for taxpayers with AGIs above $60,000 ($75,000 if married filing jointly).

If you or a loved one have questions about how your state taxes SSDI benefits or need help with the details of state taxation, you can use the chat on this page to connect with an experienced SSDI attorney.

Our team provides a free, no-obligation consultation and is ready to address any questions you may have regarding your state’s specific laws and potential tax obligations.

This method allows you to assign back pay benefits to the year they should have been received, rather than the year they were actually received.

This can help reduce your taxable income for the current year and avoid higher tax liabilities.

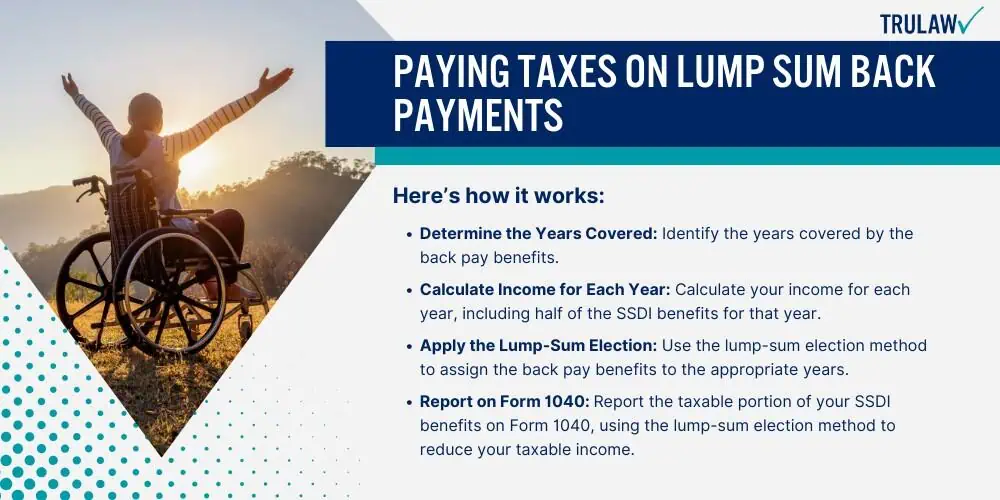

Here’s how it works:

Determine the Years Covered: Identify the years covered by the back pay benefits.

Calculate Income for Each Year: Calculate your income for each year, including half of the SSDI benefits for that year.

Apply the Lump-Sum Election: Use the lump-sum election method to assign the back pay benefits to the appropriate years.

Report on Form 1040: Report the taxable portion of your SSDI benefits on Form 1040, using the lump-sum election method to reduce your taxable income.

When you use the lump-sum election method, you recalculate the taxable part of all your benefits for the previous years (including the lump-sum payment) using that year’s income.

Then, you subtract any taxable benefits for that year that you previously reported.

The remainder is the taxable part of the lump-sum payment.

This amount is added to the taxable part of your benefits for the current year (calculated without the lump-sum payments that have been reassigned to previous years).

For example, if you received a lump sum back payment covering several prior years, you would:

Calculate the Taxable Amount for Each Year: Determine the taxable amount for each year covered by the back pay benefits, using that year’s income.

Subtract Previously Reported Taxable Benefits: Subtract any taxable benefits for those years that you previously reported.

Add to Current Year’s Taxable Benefits: Add the remaining taxable amount to the taxable part of your benefits for the current year.

By using the lump-sum election method, you can avoid paying taxes on a large lump sum in a single year and instead spread the income over the years it was intended to cover.

This can help minimize your tax liability and ensure you keep more of the benefits you’ve been given.

It is also recommended to consult with a tax professional or use tax preparation software to ensure accurate calculations and compliance with tax regulations.

If you or a loved one have received a lump sum back payment of SSDI benefits and need help addressing the tax implications, you can use the chat on this page to connect with a knowledgeable SSDI attorney.

Our team offers a free, no-obligation consultation and is available to answer any questions you may have about using the lump-sum election method to minimize your tax liability and maximize your benefits.

TruLaw — Your Trusted Resource for Social Security Disability Benefits

It’s important to be aware of the tax implications of SSDI benefits to avoid unexpected tax liabilities and ensure compliance with tax regulations.

Given the nuanced nature of SSDI taxation, recipients are strongly encouraged to consult with a tax professional or attorney to gain clarity on their individual tax circumstances and any potential liabilities.

By being proactive and informed about the tax implications of SSDI benefits, you can ensure financial stability and peace of mind.

At TruLaw, we are committed to assisting individuals in applying for or appealing an SSDI denial of their SSDI benefits.

Our experienced legal team is here to guide you through the process and ensure you receive the benefits you deserve.

Contact TruLaw using the chat on this page for a free consultation on how our law firm may be able to assist you with your SSDI benefits.

Yes, SSDI benefits can be taxable, but only if your combined income exceeds specific thresholds.

However, most SSDI recipients do not pay taxes on SSDI benefits because their income levels are typically low.

The taxability of SSDI benefits depends on the recipient’s combined income, which includes half of their SSDI benefits plus all other income and tax-exempt interest.

If this combined income exceeds specific thresholds, a portion of the SSDI benefits may be subject to taxation.

Not all Social Security Disability Insurance (SSDI) benefits are taxable.

Whether or not you’ll need to pay taxes on your SSDI benefits depends on your combined income, which includes half of your SSDI benefits plus all your other income and tax-exempt interest.

If your combined income is less than $25,000 for single filers or $32,000 for joint filers — your SSDI benefits will not be subject to federal income taxes.

While most states don’t tax Social Security Disability Insurance (SSDI) benefits, there are ten (10) states that currently do.

Following the passing of recent legislation, this list will be reduced to just eight (8) states by 2026 after Nebraska and West Virginia finish phasing out these taxes.

For states that do tax SSDI benefits, these states often have similar tax thresholds to the federal tax rules.

To determine whether you’ll need to pay tax on SSDI benefits in your state, it’s important to review the specific tax laws applicable to your state.

Attorney Jessica Paluch-Hoerman, founder of TruLaw, has over 28 years of experience as a personal injury and mass tort attorney, and previously worked as an international tax attorney at Deloitte. Jessie collaborates with attorneys nationwide — enabling her to share reliable, up-to-date legal information with our readers.

Legally Reviewed

This article has been written and reviewed for legal accuracy and clarity by the team of writers and legal experts at TruLaw and is as accurate as possible. This content should not be taken as legal advice from an attorney. If you would like to learn more about our owner and experienced injury lawyer, Jessie Paluch, you can do so here.

Fact-Checked

TruLaw does everything possible to make sure the information in this article is up to date and accurate. If you need specific legal advice about your case, contact us by using the chat on the bottom of this page. This article should not be taken as advice from an attorney.

Additional Social Security Disability Insurance resources on our website:

At TruLaw, we fiercely combat corporations that endanger individuals’ well-being. If you’ve suffered injuries and believe these well-funded entities should be held accountable, we’re here for you.

With TruLaw, you gain access to successful and seasoned lawyers who maximize your chances of success. Our lawyers invest in you—they do not receive a dime until your lawsuit reaches a successful resolution!