Eligibility Criteria for SSDI Benefits

Securing Social Security Disability Insurance (SSDI) benefits for trauma disorders hinges on specific eligibility criteria laid out by the Social Security Administration (SSA).

Applicants must demonstrate a qualifying medical condition alongside a sufficient work credit history.

Qualifying Medical Conditions

For SSDI benefits, the applicant’s trauma disorder must constitute a severe medical condition that significantly limits their ability to perform basic work activities.

This condition should be a medically determinable physical or mental impairment that a healthcare professional can objectively diagnose.

An impairment is considered severe if it prevents work for at least one full year or is expected to result in death.

Conditions are scrutinized against the SSA’s official list of medical conditions to determine eligibility.

Work Credit Requirements

To qualify for benefits, disabled workers must have accumulated the necessary work credits.

These credits are earned through work in jobs covered by Social Security, wherein some of their earnings contribute to the SSDI program.

The required number of credits depends on the applicant’s age when the disability began.

Typically, an individual needs 40 credits, 20 of which should have been earned in the last 10 years, ending with the year they become disabled.

However, younger workers may qualify with fewer credits.

Should an applicant’s earnings fall below a certain threshold, they may not meet the SSDI work credit requirement.

To summarize, an individual must have a medically verifiable and severe condition preventing them from working for a year or more, and they should have a qualifying work history that reflects sufficient contributions to the Social Security system.

The SSDI Application Process

Navigating the Social Security Disability Insurance (SSDI) application process for trauma disorders begins with meticulous preparation, especially surrounding medical evidence, and deciding between an online or in-person application approach.

Gathering Medical Evidence

A crucial step in the SSDI application process is assembling medical evidence.

Applicants should collect all relevant medical records, treatment details, and physician notes about the trauma disorder.

The Social Security Administration (SSA) requires comprehensive evidence to evaluate whether an individual’s condition meets the criteria for disability benefits.

One must ensure that their documentation establishes the disability and its impact on their ability to work.

Online and In-Person Applications

Applicants for SSDI can choose to apply online at the SSA’s official website or, if preferred, can apply in person at their local Social Security office.

The online application provides a convenient method to start the process from the comfort of one’s home, whereas an in-person application allows for direct assistance from SSA representatives.

The applicant must begin the process as soon as possible since there is a mandatory waiting period before benefits can commence.

Once the application is submitted, the wait for an initial decision can take several months, during which the SSA may request further information or clarification regarding the medical evidence provided.

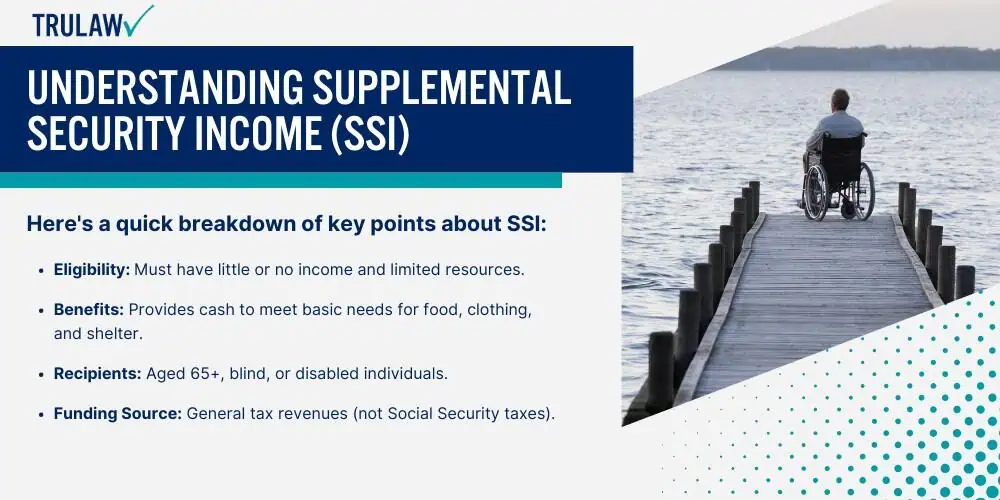

Understanding Supplemental Security Income (SSI)

Supplemental Security Income (SSI) is a federal program designed to assist individuals with limited income and resources.

SSI benefits aim to help those who are aged 65 or older, blind or disabled, and who have little or no income.

These benefits are intended to cover basic needs such as food, clothing, and shelter.

To qualify for SSI, applicants must meet specific criteria related to income and resources.

The program considers an individual’s cash, bank accounts, stocks, and U.S. government information to determine eligibility.

Here’s a quick breakdown of key points about SSI:

- Eligibility: Must have little or no income and limited resources.

- Benefits: Provides cash to meet basic needs for food, clothing, and shelter.

- Recipients: Aged 65+, blind, or disabled individuals.

- Funding Source: General tax revenues (not Social Security taxes).

It is important for individuals who believe they may be eligible to understand the application process for SSI, which includes rights during application and how to report income or changes in living arrangements.

The amount of SSI benefits an individual can receive is influenced by their income and living situation, and the maximum federal benefit rate may change yearly.

The Social Security Administration provides detailed guidelines on what constitutes income and resources and what does not count toward the limits.

Applicants and recipients of SSI must be aware of their reporting responsibilities to ensure they remain eligible for the benefits they receive.

Comparison of SSDI and SSI Benefits

When seeking disability benefits for trauma disorders, understanding the distinction between Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI) is crucial.

SSDI is designed for individuals who have worked and paid into the Social Security system through taxes.

The benefit amount a person receives is based on their earnings record.

Conversely, SSI benefits are need-based and do not depend on an individual’s work history but rather on financial need.

Eligibility Criteria SSDI SSI Work Credits Required Yes No Income Considerations Evaluates past earnings Must have limited income and resources Resource Limitations None Yes, assets cannot exceed $2,000 for individuals or $3,000 for couples.

With regards to trauma disorders, applicants must provide medical evidence demonstrating their condition impairs their ability to work.

Both SSI and SSDI programs require a disability that is expected to last at least one year or result in death.

Other income can affect the amount of benefits received.

SSI benefits may decrease if the individual has other income, while SSDI benefits remain generally unaffected by other income sources.

However, engaging in substantial gainful activity can impact eligibility for both programs.

Regarding healthcare coverage, SSDI recipients may become eligible for Medicare after a two-year waiting period, whereas SSI beneficiaries may be eligible for Medicaid immediately.

It’s important to note that although both forms of assistance provide vital support, a key difference is that SSI beneficiaries must continue to meet certain low-income criteria to maintain their benefit status.

Financial Aspects of Disability Benefits

When individuals secure Social Security Disability Insurance (SSDI) benefits for trauma disorders, they are navigating a financial landscape shaped by predetermined government guidelines.

The fiscal ramifications, specifically regarding payment calculations and the intersection with retirement age, are crucial for beneficiaries to understand.

Payment Calculations

The amount of cash benefits an individual receives from SSDI is closely linked to their past income and the Social Security taxes they’ve paid into the system.

To determine the benefit amount, the Social Security Administration (SSA) utilizes a formula that considers the average indexed monthly earnings (AIME) and applies a multi-tiered calculation.

Generally, the higher the AIME, the higher the monthly disability payment, though it’s subject to a maximum cap established by SSA.

Impact on Retirement Age

SSDI benefits can also influence an individual’s retirement funds and the age at which they opt for retirement.

When beneficiaries reach full retirement age, their disability benefits automatically convert into retirement benefits, but the amount typically remains the same.

It’s important to note that taking disability benefits does not reduce their future Social Security retirement benefits; however, both SSDI and Social Security retirement are rooted in the recipient’s earnings history and the length of time they’ve contributed to the Social Security fund.

Rights and Protections for Beneficiaries

Beneficiaries of Social Security Disability Insurance (SSDI) for trauma disorders are entitled to specific rights and protections.

These safeguards ensure that recipients and their certain family members maintain financial security while potentially gaining access to work incentives.

Work Incentives and Subsidies

Social Security Disability Insurance offers various work incentives and subsidies to encourage beneficiaries to explore employment without immediate risk to their benefits.

Two key incentives include:

- Trial Work Period (TWP): Gives beneficiaries the chance to work for at least nine months in a rolling 60-month period without losing benefits, regardless of earnings.

- Extended Period of Eligibility (EPE): After the TWP, for the next 36 months, beneficiaries can receive SSDI for any month where earnings fall below the Substantial Gainful Activity (SGA) level.

These incentives are designed to support the disabled individual’s transition back into the workforce, providing a safety net while they test their ability to work.

Family Members’ Benefits

SSDI not only supports individuals with trauma disorders but also extends benefits to certain family members.

Eligible members can include:

- A spouse aged 62 or older

- A spouse of any age caring for a child under 16 or disabled

- Unmarried children, including adopted children or, in some cases, stepchildren or grandchildren under 18 (or 19 if still in high school)

Qualified family members may receive up to 50% of the disabled beneficiary’s benefit amount, though a family limit usually ranging from 150% to 180% of the beneficiary’s benefit applies to the total amount payable to a family.

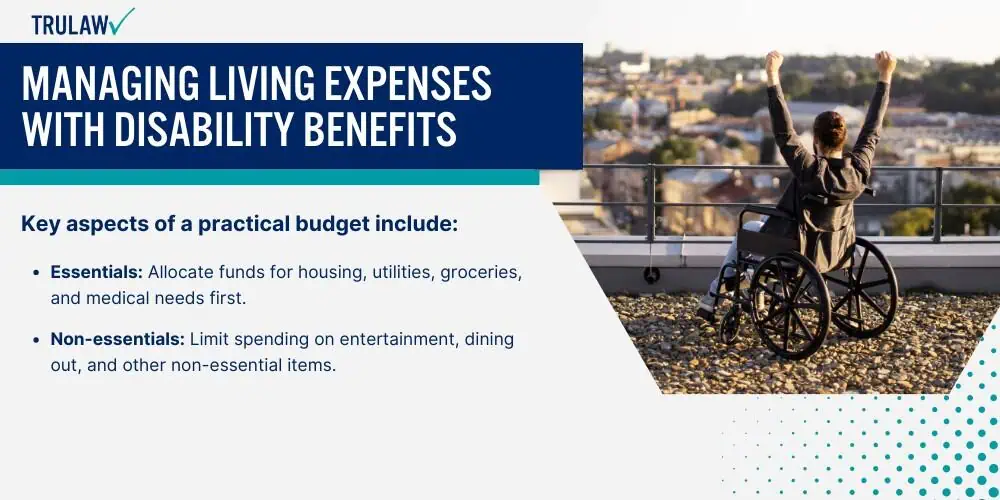

Managing Living Expenses with Disability Benefits

Living with a trauma disorder can be challenging, and navigating the financial implications is an essential part of managing one’s living situation.

Individuals receiving Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI) benefits often have to adjust their budgeting strategies to accommodate their limited income.

Eligible individuals, especially those who are severely impaired, need to be strategic about their financial resources to ensure their disability benefits cover their monthly expenses.

Creating a budget is critical for beneficiaries to manage their money effectively.

Key aspects of a practical budget include:

- Essentials: Allocate funds for housing, utilities, groceries, and medical needs first.

- Non-essentials: Limit spending on entertainment, dining out, and other non-essential items.

For households with a severely impaired member, keeping track of every dollar is vital.

Beneficiaries must consider their living situation, as some may qualify for housing assistance programs, reducing the portion of their benefits that goes toward rent or mortgage.

Since many recipients have limited income, they should explore additional resources such as food assistance programs or subsidized medical services.

To maximize the benefits of their SSDI or SSI, beneficiaries can explore various assistance programs that help in reducing everyday living expenses.

These resources can significantly stretch their limited income:

- Housing: Look into federally funded housing programs.

- Medical: Investigate Medicaid or state-sponsored health programs.

- Food: Consider the Supplemental Nutrition Assistance Program (SNAP).

Every dollar saved from these resources can be redirected to other necessary expenses, ensuring that the monthly SSDI or SSI benefits provide a security net for these individuals.

Careful planning and knowledge of available assistance programs are integral to managing living expenses on disability benefits.

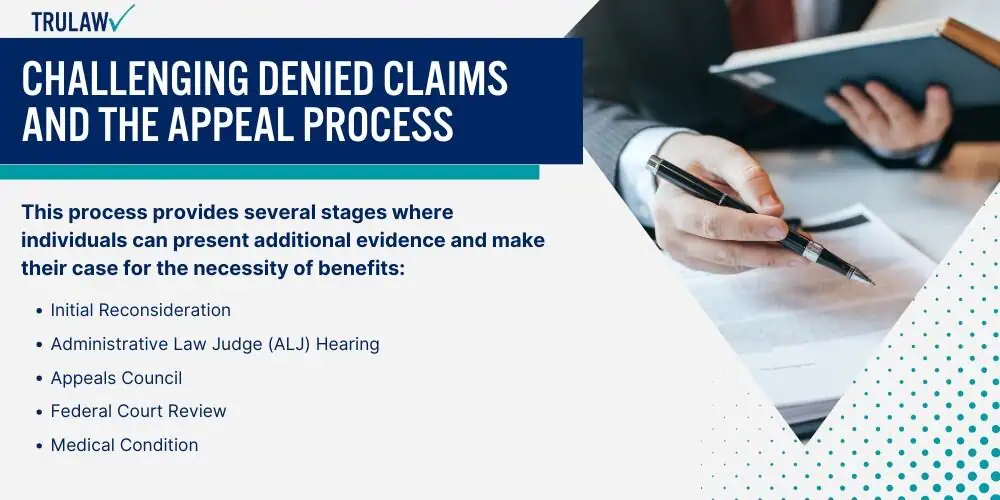

Challenging Denied Claims and the Appeal Process

When an individual’s claim for Social Security Disability Insurance (SSDI) benefits for trauma disorders is denied, they have the right to challenge the decision.

The appeals process for Social Security benefits is a crucial step for those who have been initially denied.

This process provides several stages where individuals can present additional evidence and make their case for the necessity of benefits:

- Initial Reconsideration: Start with having your file reviewed anew by someone not initially involved.

- Administrative Law Judge (ALJ) Hearing: Has your request for reconsideration been unsuccessful? Request a hearing. Present new evidence and expert testimonies here.

- Appeals Council: After an ALJ decision, if still unfavorable, seek a review by the Social Security’s Appeals Council.

- Federal Court Review: As a final step, consider filing a lawsuit in a federal district court.

- Medical Condition: Ensure thorough documentation of your trauma disorder.

- Substantiation: Bolster your case with medical expert opinions and treatment records.

The claimant must prove that the trauma disorder significantly impairs their ability to engage in substantial gainful activity.

The burden of proof lies with the claimant to demonstrate the severity of their condition and how it hinders their work life.

The SSDI application and appeal process are complex, but understanding the steps and preparing thoroughly can maximize one’s chances of receiving cash benefits.

Patience and detail are essential as several factors, including the extent of the disability and previous work experience, are considered during the benefit determination.

Impact of Disability on Employment and Earnings

When an individual is affected by a trauma disorder, their ability to engage in employment and the potential earnings they can generate are often significantly impacted.

Understanding the governmental thresholds and the long-term effects is critical for those navigating Social Security Disability Insurance (SSDI).

Substantial Gainful Activity

The Social Security Administration (SSA) uses the term Substantial Gainful Activity (SGA) to describe a level of work activity and earnings.

For individuals with disabilities, earning more than the SGA monthly threshold can disqualify them from receiving SSDI benefits. In 2023, the SGA amount for non-blind individuals is $1,350 monthly.

For those who are statutorily blind, the threshold is higher, set at $2,260.

These amounts are adjusted annually to reflect changes in national wages.

According to Social Security guidelines, a person must have a medical condition that meets the strict definition of disability and be unable to work above the SGA due to that disability to qualify for SSDI receive benefits.

Effects on Future Employment

Trauma disorders can have a profound effect on an individual’s future employment prospects and earnings.

Being on SSDI does not necessarily mean an individual cannot work again, but returning to work can be a complex process. Working while receiving benefits can raise concerns about how the earnings might affect their SSDI eligibility.

Although disabled workers may attempt to return to work, the uncertainty of maintaining consistent employment due to their disability often leads to reduced lifetime earnings.

SSDI provides a structure through the Ticket to Work program, which supports disability beneficiaries aiming to transition back into the workforce.

However, if their earnings fall due to an inability to sustain work, the individuals may return to the program for support.

Planning for the Future: Disability and Retirement

Understanding how Social Security Disability Insurance (SSDI) transitions to retirement benefits and Medicare coverage is essential for beneficiaries, especially as they retire.

Strategic planning can ensure a stable transfer and maximized benefits during this significant life change.

Transition from SSDI to Retirement Benefits

When SSDI recipients reach their full retirement age, which varies depending on their birth year, their SSDI benefits automatically convert to retirement benefits without reducing monthly payments.

For those born after 1960, the full retirement age is 67.

The amount they receive typically remains the same, embodying what they would be entitled to at full retirement age based on their earnings record.

It’s important to note that working while receiving SSDI is possible.

Beneficiaries who continue to work might be able to increase their future retirement benefits.

Earnings can replace lower-earning years in their Social Security earnings history, potentially resulting in a higher benefit calculation.

Medicare Coverage for SSDI Recipients

Medicare coverage begins 24 months after an individual’s SSDI benefits start.

They are automatically enrolled in Medicare Part A and Part B.

Individuals can refuse or buy additional coverage like Medicare Part D for prescription drugs.

Medicare continues seamlessly for beneficiaries approaching retirement age as long as they are enrolled before reaching 65.

Although most individuals become eligible for Medicare at 65, those with SSDI are granted earlier access due to their disability status, ensuring continuous healthcare coverage.

Both transitions—into retirement benefits and continued Medicare coverage—are designed to be smooth and beneficial for SSDI recipients.

Through this process, benefits continue, and healthcare coverage is maintained, helping to safeguard against financial disruptions as individuals transition from a focus on their disability to retirement.

Support Services and Resources for the Disabled

Individuals contending with trauma disorders may find a wealth of support services and resources through various disability programs.

The Social Security Administration (SSA) is pivotal, offering initiatives like Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI).

Eligibility for these programs typically requires that the disabled person has enough work history and a medical condition that fits the SSA’s definition of disability.

The disability must be expected to last at least one month or be terminal.

One can use tools such as the Benefit Eligibility Screening Tool to determine eligibility for SSI.

The Social Security Administration (SSA) offers several resources to assist disabled workers in reporting changes that could impact their benefits, such as fluctuations in income or improvements in their disability status.

These resources are designed to ensure that individuals are well-informed and adequately supported throughout the process:

- Educational Resources: Individuals with disabilities can access information sessions and materials explaining their rights and the various programs for which they may be eligible.

- Legal Support: The SSA encourages representation by a qualified Social Security Disability lawyer to assist in navigating the complexity of claims and improving the prospects of approval.

For additional support, non-profit organizations and advocacy groups provide services tailored to disabled individuals.

These can include counseling, job training, and assistance with benefits applications.

Workers with disabilities must submit periodic reports to the SSA reflecting their current income and work status to maintain their benefits.